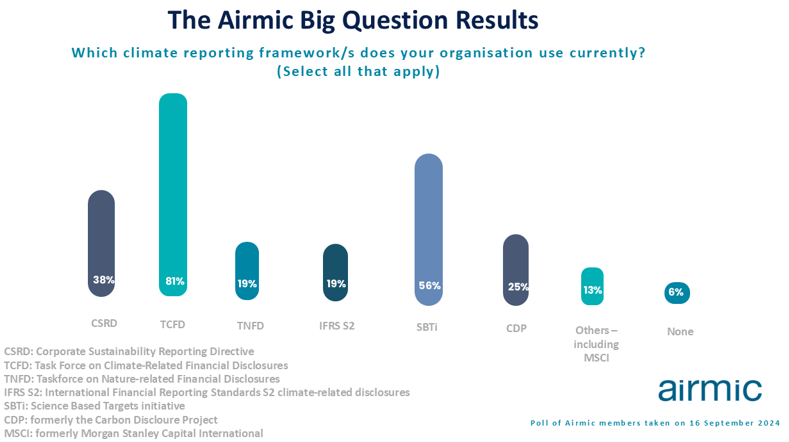

The vast majority (81%) of risk professionals are using the Task Force on Climate-Related Financial Disclosures among their climate reporting frameworks, while a further 56% use the Science Based Targets initiative – despite the carbon offset controversy surrounding SBTi earlier this year.

These are the key findings of Airmic’s latest ‘Big Question’ poll of risk professionals focused on the process of producing climate disclosures.

While the choice of reporting framework is generally driven by jurisdictional or parent entity requirements, respondents also cited strategic and operational commitments, as well as reputational and stakeholder considerations, among the factors influencing their decision.

Commenting on the findings, Hoe-Yeong Loke, head of research, Airmic, said: “There is an important role for climate reporting frameworks in aligning the activities within an organisation, as well as aligning climate ambitions across the corporate sector with international goals. However, bodies such as the Financial Reporting Council are finding that many climate disclosures produced by organisations have been unclear in terms of concrete actions and milestones to meet the targets they have set. The disclosures also tend to be regarded as a tick-box exercise. Organisations should assess their climate risks more realistically and carefully.”

Leigh-Anne Slade, head of media, communications and Interest Groups, Airmic, added: “The challenge facing risk professionals is balancing commercial profit against doing the ‘right thing’ for climate change. They can steer their organisations towards using the right metrics and incremental targets, bringing out not just the risks but also the opportunities. Airmic is actively engaging members through our special interest groups to share best practices, which will ultimately guide their entire business toward achieving net zero."

The other frameworks used by Airmic members for climate reporting include:

Corporate Sustainability Reporting Directive (38%)

Taskforce on Nature-Related Financial Disclosures (19%)

International Financial Reporting Standards S2 Climate-Related Disclosures (19%)

Science Based Targets Initiative (56%)

CDP Worldwide (25%)

Others (including MSCI) (13%)

The TCFD framework is endorsed by the UK Government, and is mandatory for large entities in the private sector.

Printed Copy:

Would you also like to receive CIR Magazine in print?

Data Use:

We will also send you our free daily email newsletters and other relevant communications, which you can opt out of at any time. Thank you.

YOU MIGHT ALSO LIKE